In December 2024, The Japan National Tax Agency (NTA) has recently issued an update correction to Form of Statement Concerning Foreign Tax Credit for an individual resident taxpayer for 2022 calendar year and thereafter. This correction is concerning foreign income taxes on distribution of collective investment trust income.

1. Understanding Japan’s Foreign Tax Credit System

Japan’s tax system is designed to mitigate the double taxation of income that might otherwise be taxed both in Japan and in another country. The foreign tax credit is a critical component of this system, providing relief by crediting foreign taxes paid against Japanese tax liabilities. If a resident is subject to foreign income taxes under the laws and regulations of a foreign country with respect to foreign source income, the resident shall, for the purpose of preventing international double taxation, credit the creditable foreign income tax against his/her income tax amount for the year up to the maximum credit amount specified by law. The maximum creditable amount of income tax for the year is stipulated by law.

2. Adjusted Foreign Tax Equivalent Credit at the Time of Distribution

Where a collective investment trust owns foreign company’s stocks or bonds and dividend income or interest income are subject to foreign income taxes, the collective investment trust deducts the foreign income taxes from Japan withholding income taxes on distributions the collective investment trust makes to eliminate double taxation. A resident taxpayer is allowed to credit the foreign income taxes the collective investment trust deducted from the Japan withholding income taxes on distributions against his or her income tax amount when files personal income tax return subject to limitation to settle double taxation properly. This tax credit system was implemented in 2018 Tax Reform.

3. Incorrect form of “Statement of Foreign Tax Credit

The error discovered in the Calculation of Tax Credit Limit section of the detail sheet involved incorrect instructions for calculating the base amounts used in determining tax credits. Previously, the forms guided taxpayers to use income tax amount before deducting Adjusted Foreign Tax Equivalent Credit at the Time of Distribution , which could result in incorrectly high claims for tax credits. The correct procedure, as clarified in the updated form, requires taxpayers to calculate the creditable limit using income tax amount after deducting Adjusted Foreign Tax Equivalent Credit at the Time of Distribution . This ensures that the calculations align accurately with the tax laws, preventing discrepancies in tax payments. Details of update is as below:

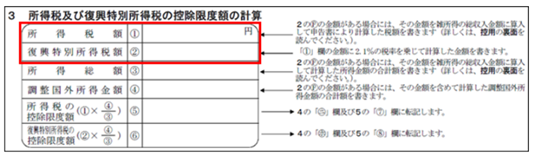

- Error in the section Calculation of the Tax Credit Limit for Income Tax and Special Reconstruction Income Tax on the Foreign Tax Credit Detail Sheet (for Residents) (for fiscal year Reiwa 2 and beyond).

![Calculation of the Tax Credit Limit for Income Tax and Special Reconstruction Income Tax on the Foreign Tax Credit Detail Sheet (for Residents) (for fiscal year Reiwa 2 and beyond)]()

Source: “Foreign Tax Credit Detail Sheet (for Residents)”, National Tax Agency of Japan (NTA)

- The section describes incorrect and correct content for documenting the "Income Tax Amount「所得税額」(①) and "Special Reconstruction Income Tax Amount"「復興特別所得税額」 (②) fields. The explanation concerns the instructions on the back of the form detailing how these amounts should be recorded.

- Below table outlines the errors and the correct methods for filling out specific fields related to income tax amounts on the Japanese tax form, especially when adjustments are needed due to specific tax credits.

| Section |

Incorrect |

Correct |

|

|

The Standard Income Tax Amount field amount from the Tax Calculation section of the table 1 in Tax Return is transposed to Income Tax Amount(column①).

|

In column ➀,Base Income Tax Amount column in the “Calculation of Taxes” section of Table 1 of the tax return.

However, if the deduction for the amount equivalent to foreign taxes adjusted at the time of distribution is applied, prepare the “Statement Concerning Deduction for Foreign Tax Equivalent at the Time of Distribution” first, and then post the amount in column 3(7) of the “Statement Concerning Deduction for Foreign Tax Equivalent Adjustment at the Time of Distribution

|

Special Reconstruction Income Tax Amount (②)

|

Calculate the amount by applying a 2.1% tax rate to the amount in the column ①.

|

In column (2), post the amount shown in the “Special Reconstruction Income Tax Amount” column in the “Calculation of Taxes” section of Schedule 1 of the tax return.

However, if the deduction for the amount equivalent to foreign taxes adjusted at the time of distribution is applied, post the amount shown in 3(9) of the “Statement Concerning Deduction for Foreign Tax Equivalent Adjustment at the Time of Distribution”.

|

4. Impact and Corrective Actions by the NTA

The NTA has acted swiftly to address this issue by revising the affected forms and updating the related software systems to prevent similar errors in the future. These corrections are crucial not only for maintaining the integrity of the tax system but also for ensuring that businesses can rely on the provided documentation to accurately compute their tax obligations.

5. Implementation and Compliance

The revised forms were made available as of December 6, Reiwa 6 (2024), with the updates to software systems scheduled for completion by January 6, Reiwa 7 (2025). Taxpayers are encouraged to adopt these updated forms immediately to ensure compliance and to avoid errors in upcoming tax filings.

【Correction and Apology】

April 15, 2025

We have made corrections to ensure the accuracy of the content and have updated certain points accordingly.

We sincerely apologize for any confusion or inconvenience this may have caused.